You're paying more

in interest than

you realise.

The IMA Planner Debt Calculator gives you an exact debt-free date, a month-by-month payment plan, and shows which strategy saves you the most money. Try the live demo free.

See your debt-free date right now.

Enter your real numbers. Same logic as the full template — free, instant, no strings.

debt-free

debt-free date

you'll pay

minimum only

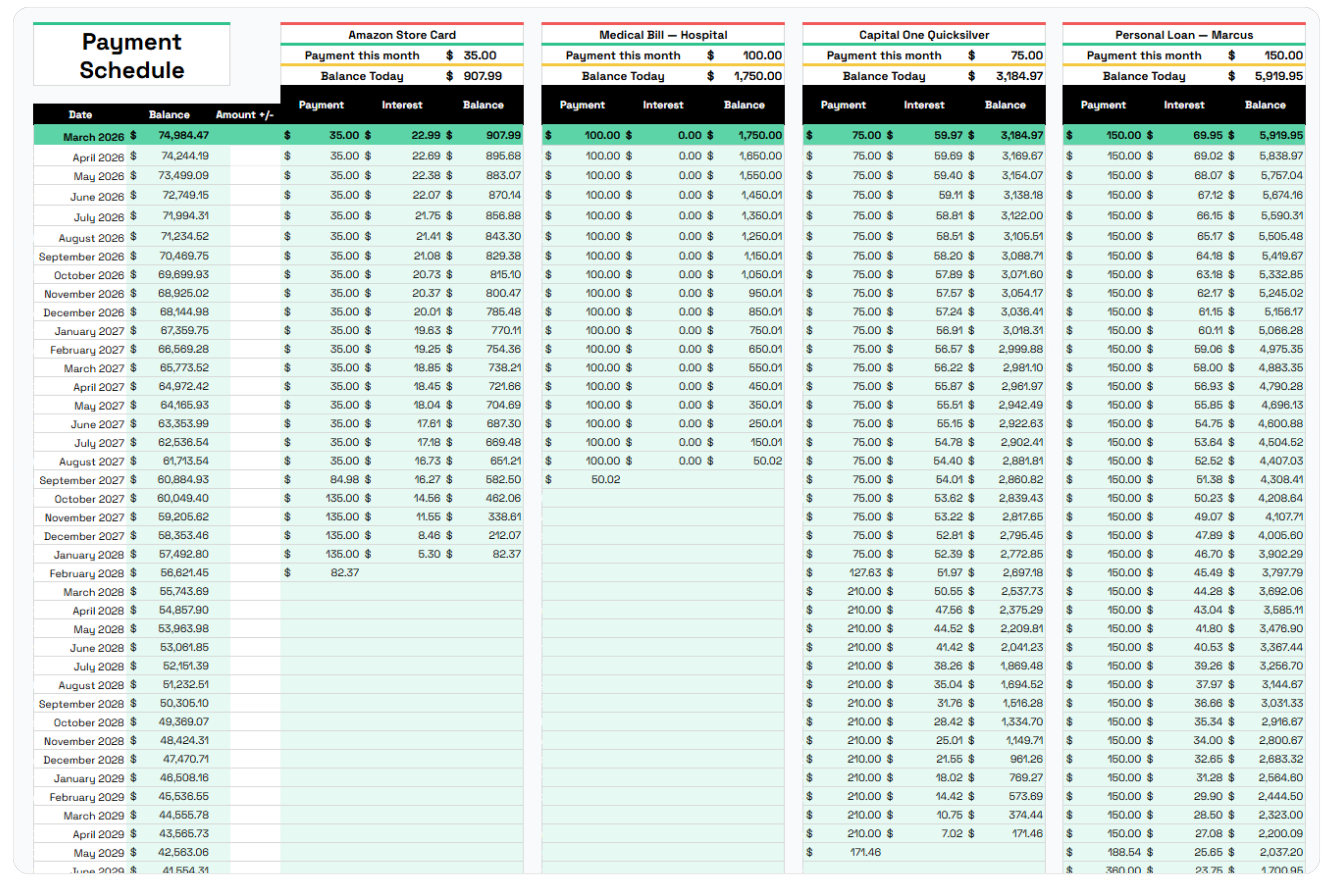

Track up to 10 debts, auto-sort by strategy, see the complete payment schedule to your last payment.

Why not just use a

free calculator?

Honest answer. Here's exactly what free tools give you — and what they don't.

Every month from today to your last payment — all calculated automatically.

Minimum payments are

a very expensive trap.

Snowball or Avalanche?

Both beat doing nothing by thousands.

The difference between the two methods is often under $1,300. What matters is picking one and starting. This calculator shows you both.

- Quick wins build real psychological momentum

- Fewer debts to track sooner — reduces overwhelm

- Proven to improve follow-through vs math-only approaches

- Backed by Federal Reserve consumer finance research

- Minimizes total interest paid — saves up to 4.3% more

- Typical saving of $2,000–$4,000 on $28k debt

- Faster payoff date in most multi-debt scenarios

- Especially powerful at today's 20%+ APRs

Everything calculated.

Nothing to figure out.

Enter your debts once. The spreadsheet handles sorting, scheduling, and projecting — all automatically.

Start in under 10 minutes.

No spreadsheet experience needed. If you can type a number, you can use this.

The numbers behind the strategy.

"The Snowball method offers significant psychological advantages in motivation and habit-forming — making it a very close competitor to Avalanche even when the math slightly favors the alternative."

Federal Reserve Survey of Consumer Finance — debt payoff strategy researchBuilt for anyone

with a balance to clear.

The people who stick with it

actually pay it off.

What a year of logging payments in the spreadsheet looks like — month by month, balance going to zero.

Every question you're

probably thinking.

Your debt-free date is

one spreadsheet away.

This costs less than one day of interest on your debt. If it helps you pay off even one month earlier, it pays for itself a hundred times over.